Money And Household Management: A Comprehensive Guide To Mastering Your Finances

Money and household management is more than just balancing numbers—it’s about creating a life of stability, growth, and security for you and your family. Whether you’re just starting out or looking to refine your financial strategies, understanding how to manage money within your household is crucial. Think of it as the foundation that supports everything else in your life. So, how do you get started? Let’s dive in and break it down step by step.

Managing finances can seem overwhelming at first, especially when you’re juggling multiple responsibilities. But don’t stress—it’s all about taking small, consistent steps. In this guide, we’ll walk you through everything from budgeting basics to long-term financial planning. By the end, you’ll have the tools and confidence to take control of your money and household.

Now, let’s be real here—money isn’t just about math. It’s about mindset, habits, and priorities. Whether you’re trying to save for a dream vacation, pay off debt, or build a rainy-day fund, having a solid plan in place is key. This article is packed with practical tips, real-life examples, and expert advice to help you navigate the world of money and household management. Ready to get started? Let’s go!

- Boost Your Secondhand Stoffwechsel A Comprehensive Guide To Metabolism Transformation

- Asia Markt Offenburg Your Ultimate Guide To Exploring The Best Asian Market In Town

Understanding the Basics of Money and Household Management

Before we dive into the nitty-gritty, let’s talk about the fundamentals. Money and household management isn’t rocket science, but it does require a clear understanding of your income, expenses, and financial goals. Think of it as building a house—you need a strong foundation before you start adding walls and windows.

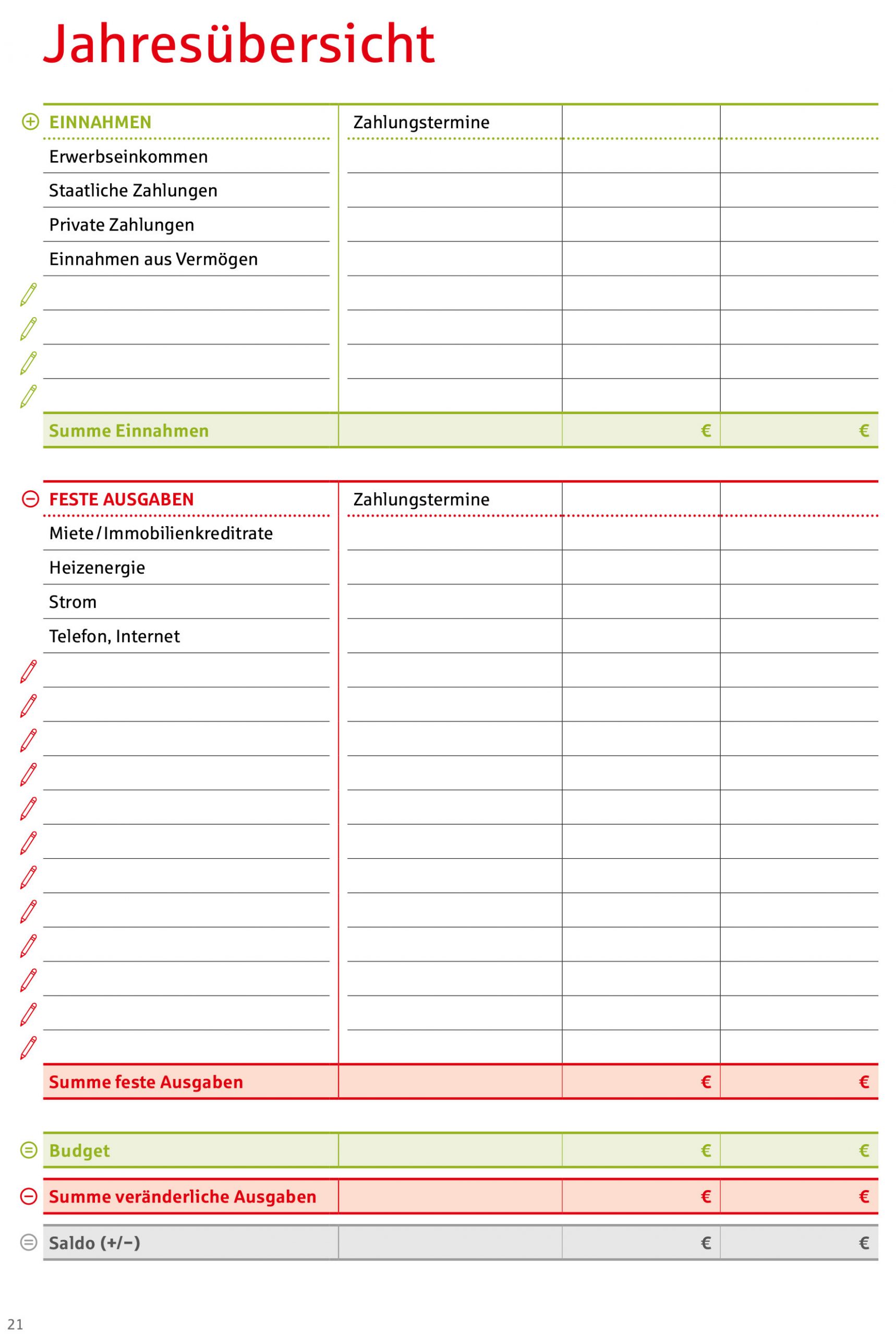

Creating a Budget That Works for You

One of the most important steps in managing money and household expenses is creating a budget. But here’s the thing—not all budgets are created equal. Some people thrive on detailed spreadsheets, while others prefer a more relaxed approach. The key is finding what works for you.

- Track your monthly income and expenses.

- Identify areas where you can cut back.

- Set realistic financial goals, whether it’s saving for a down payment or reducing credit card debt.

Remember, a budget isn’t about restricting yourself—it’s about giving your money a purpose. When you know where your money is going, you’re less likely to waste it on unnecessary expenses.

- Hot Lava A Fiery Journey Through Natures Molten Wonders

- Bensheimer Hof A Hidden Gem In The Heart Of Bavaria

Why Budgeting Matters in Money and Household Management

Budgeting isn’t just for people who are struggling financially. Even if you’re doing well, having a budget helps you stay on track and avoid unexpected surprises. Think of it as your financial GPS—it keeps you headed in the right direction.

According to a study by the National Endowment for Financial Education, only 41% of Americans have a budget. That means the majority of people are flying blind when it comes to their finances. Don’t be one of them—take control of your money today!

Building a Strong Financial Foundation

Once you’ve got the basics down, it’s time to focus on building a strong financial foundation. This includes everything from emergency funds to retirement savings. Let’s break it down.

Setting Up an Emergency Fund

An emergency fund is like a safety net—it’s there to catch you when life throws unexpected curveballs. Whether it’s a medical emergency, car repair, or job loss, having a stash of cash set aside can make all the difference.

Experts recommend saving at least three to six months’ worth of living expenses. But don’t get overwhelmed—if you’re just starting out, aim for $1,000 and build from there. The important thing is to start somewhere.

Maximizing Your Retirement Savings

Retirement might seem far away, but trust me—it’s never too early to start planning. The earlier you start saving, the more time your money has to grow thanks to the power of compound interest.

If your employer offers a 401(k) match, take advantage of it. It’s essentially free money! And if you’re self-employed, consider opening an IRA or Solo 401(k). Whatever route you choose, the key is consistency—make saving for retirement a priority.

Debt Management Strategies

Let’s face it—most of us have some form of debt, whether it’s credit cards, student loans, or a mortgage. But don’t let it weigh you down. With the right strategies, you can take control of your debt and work toward financial freedom.

The Debt Snowball Method

The debt snowball method is a popular approach developed by financial expert Dave Ramsey. Here’s how it works:

- List all your debts from smallest to largest.

- Focus on paying off the smallest debt first while making minimum payments on the others.

- Once the smallest debt is gone, roll that payment into the next smallest debt, and so on.

This method is all about momentum—each debt you pay off gives you a sense of accomplishment and motivation to keep going.

The Debt Avalanche Method

If you’re more numbers-driven, the debt avalanche method might be for you. With this approach, you focus on paying off the debt with the highest interest rate first. While it may take longer to see results, you’ll save more money in the long run.

Ultimately, the best method is the one that works for you. Whether you choose snowball or avalanche, the key is consistency and discipline.

Investing in Your Future

Investing is one of the most powerful ways to grow your wealth over time. But it can also be intimidating if you’re new to the game. Let’s demystify the process and break it down into manageable steps.

Understanding Different Types of Investments

From stocks and bonds to mutual funds and real estate, there are plenty of options when it comes to investing. Here’s a quick overview:

- Stocks: Ownership shares in a company. High risk, high reward.

- Bonds: Loans to a company or government. Lower risk, lower return.

- Mutual Funds: Pooled investments managed by a professional.

- Real Estate: Investing in property, whether it’s rental homes or flipping houses.

The key is diversification—don’t put all your eggs in one basket. By spreading your investments across different asset classes, you reduce your risk and increase your chances of long-term success.

Getting Started with Investing

If you’re new to investing, don’t worry—it’s easier than you think. Start by educating yourself—there are plenty of books, podcasts, and online courses to help you get started. Then, open an investment account through a brokerage firm or robo-advisor.

Remember, investing is a marathon, not a sprint. Stay focused on your long-term goals and don’t let short-term market fluctuations derail your plan.

Managing Household Expenses

Now that we’ve covered the big-picture stuff, let’s talk about the day-to-day expenses that make up your household budget. From utilities to groceries, there are plenty of ways to save money without sacrificing quality.

Cutting Costs Without Sacrificing Comfort

Here are a few simple tips to help you save money on household expenses:

- Switch to energy-efficient light bulbs.

- Shop for groceries with a list and stick to it.

- Cancel subscriptions you don’t use.

- Negotiate better rates on your internet and cable bills.

Small changes can add up to big savings over time. The key is being intentional with your spending and looking for areas where you can cut back without impacting your quality of life.

Utilizing Technology to Simplify Household Management

There are plenty of apps and tools available to help you manage your household finances. From budgeting apps like Mint and YNAB to bill-paying services like PayPal and Zelle, technology can make your life a lot easier.

Take advantage of these tools to streamline your finances and stay organized. The less time you spend worrying about money, the more time you can focus on the things that truly matter.

Long-Term Financial Planning

Managing money and household expenses isn’t just about today—it’s about building a secure future for yourself and your family. Let’s talk about some strategies for long-term financial success.

Setting Financial Goals

Whether you’re planning for a child’s education, buying a home, or retiring early, setting clear financial goals is essential. Write them down, break them into actionable steps, and track your progress along the way.

Remember, goals should be SMART—specific, measurable, achievable, relevant, and time-bound. The more specific your goals, the easier it is to stay focused and motivated.

Reviewing and Adjusting Your Plan

Your financial situation will change over time, so it’s important to regularly review and adjust your plan. Life events like marriage, children, or career changes can all impact your financial goals. Stay flexible and be willing to adapt as needed.

Common Mistakes to Avoid

Even the best-laid plans can go awry if you’re not careful. Here are a few common mistakes to avoid when managing money and household expenses:

- Not having a budget.

- Ignoring debt.

- Not saving for emergencies.

- Trying to keep up with the Joneses.

Avoid these pitfalls by staying disciplined and focused on your long-term goals. Remember, financial success is a journey, not a destination.

Conclusion: Take Control of Your Finances Today

Managing money and household expenses can seem daunting, but with the right tools and mindset, it’s completely achievable. From creating a budget to investing in your future, every step you take brings you closer to financial freedom.

So, what’s next? Start by taking one small action today—whether it’s setting up a budget, paying off a debt, or opening an investment account. Consistency is key, so don’t get discouraged if progress feels slow at first. Keep moving forward, and before you know it, you’ll be well on your way to mastering your finances.

And don’t forget to share this article with friends and family who might benefit from it. The more we talk about money and household management, the better equipped we’ll all be to create a brighter financial future. Let’s do this together!

Detail Author:

- Name : Imani Runolfsson

- Username : dawson09

- Email : orath@hansen.com

- Birthdate : 1981-05-10

- Address : 351 Hoeger Land Suite 389 Pollichport, RI 34070

- Phone : +1 (463) 395-6015

- Company : Hill Ltd

- Job : Financial Manager

- Bio : Adipisci vitae et explicabo iusto non. Corrupti quis voluptatem quas laudantium delectus. Aliquam voluptatibus omnis distinctio dolore hic eaque.

Socials

linkedin:

- url : https://linkedin.com/in/jaquan.kuhic

- username : jaquan.kuhic

- bio : Neque ut ratione neque esse.

- followers : 6178

- following : 2845

twitter:

- url : https://twitter.com/jaquan_xx

- username : jaquan_xx

- bio : Id qui assumenda aut tempora ut eum. Voluptatem itaque enim voluptas non mollitia ex quia. Provident recusandae esse cumque voluptate.

- followers : 6180

- following : 1963

{kind=link}